AUS

AUS

US

US

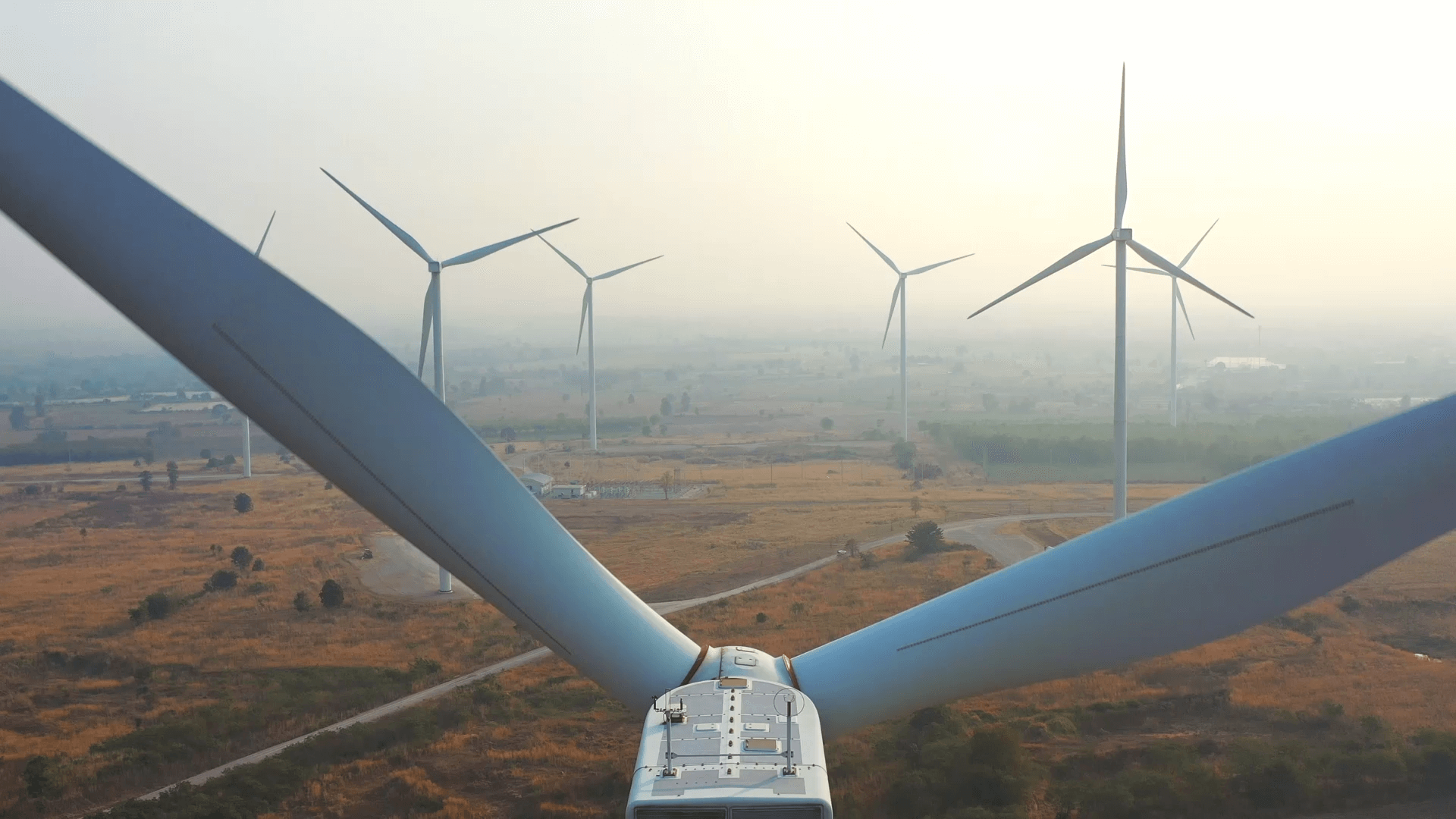

Driving growth in onshore wind: Opportunities and challenges to 2030

Discover how the UK’s onshore wind sector is evolving. Business Development Manager, Will Russell shares key insights from the Onshore Wind Conference 2025, covering the latest policy changes, investment trends, and what’s next for the UK’s onshore wind sector.

The onshore wind sector is at a pivotal moment, and last week’s Onshore Wind Conference in Edinburgh was a powerful reminder of the innovation, collaboration and momentum driving it forward.

Michael Shanks, Minister for Energy, made it clear: “Clean power is the economic opportunity of the 21st century, and onshore wind is critical to this mission”. His words underscore the strategic importance of onshore wind, not just as a renewable energy source, but as a driver of economic growth, community benefit, and national energy security.

A decade of change: How policy shifts have enabled growth

Over the past year, the onshore wind sector has seen promising growth, driven by a new government strategy and an increased pipeline of projects, with a goal to deliver 27-29GW by 2030.

After nearly a decade of stalled projects following the Conservative Government’s de facto ban on onshore wind in England, the newly elected Labour Government lifted the ban in July 2024 as one of its first actions. This policy shift sent a clear signal of support for the sector and the growth of renewables.

Since then, the Government has continued to reinforce its commitment to a cleaner energy future. Its Clean Power 2030 targets set a clear pathway to a decarbonised power system by 2030, aiming to double current onshore wind capacity. This ambition is supported by a new, dedicated strategy, the Onshore Wind Taskforce Strategy, which outlines 42 actions to accelerate deployment, and a newly established Onshore Wind Council to oversee implementation, both driving tangible progress over the past year.

Overcoming barriers: Challenges to deliverability

However, while the sector is growing, deliverability remains essential to achieving renewable targets, and challenges persist. Several projects are stuck in the pipeline due to slow planning and consenting processes, with restrictions from aviation and the Ministry of Defence, as well as supply chain disruptions and grid connection bottlenecks.

Investment certainty also remains a concern. The rejection of zonal pricing in favour of reformed national pricing brought some clarity, but it leaves much open to potential reforms, creating uncertainty for developers. Alongside this, rising TNUoS charges add further volatility, with forecasts only increasing in the years to come. Addressing these issues will be critical to sustaining growth.

Collaboration as a driver of progress

Despite these challenges, progress continues, and none of it would have been possible without collaboration. This was a strong message highlighted throughout the conference, reflected in joint efforts in technology, project delivery, and stakeholder engagement.

Yet, public perception remains a challenge, with anti-wind rhetoric and polarised opinions still present. The sector must actively demonstrate the value of onshore wind: reducing energy bills, creating jobs, supporting skills development, strengthening community benefits, and improving long-term energy security.

Looking ahead: CfDs and the next wave of investment

So with all this in mind, what’s next for onshore wind? Chris Stark, the UK Government’s Head of Mission Control for Clean Power 2030, described the period ahead as a “supercycle of investment for onshore wind,” highlighting that the upcoming Contracts for Difference Allocation Round 7 (CfD AR7) auction will be a “very high stakes moment” for the sector and the renewables industry as a whole.

The latest AR7 reforms have been welcomed by all, including extended contract terms from 15 years to up to 20 years, and the introduction of repowered onshore wind projects. CfDs remain the primary route to market for developers, so this auction round will be critical to delivering the projects at the scale required to stay on track for 2030.

But, not all projects will secure a CfD contract, whether this be due to budget constraints, timing, or the need for diversification. CfDs offer fixed, government-backed pricing with low risk and long-term certainty, meanwhile Corporate Power Purchase Agreements (CPPAs) provide flexible, market-linked pricing and optional hedging tools. Developers are increasingly combining CfDs with CPPAs across their portfolios to balance risk and navigate policy uncertainty. This hybrid approach supports financing and builds resilience in a shifting policy landscape.

Achieving renewable growth requires not just infrastructure, but investment supported by route to market tools that reduce risk, secure pricing, and enable long-term planning.

At SmartestEnergy, we support both CfDs and CPPAs, helping generators, and corporates structure flexible, bankable solutions in a rapidly evolving market. I had the pleasure of exploring these strategies in more detail during the panel session ‘Rethinking Project Finance’ at the Onshore Wind Conference 2025 last week.

Secure a route to market for your onshore wind project

Explore the practical insights from my presentation on CfDs, CPPAs, and hybrid approaches to accelerate your projects and secure long-term growth.

Discover more

SmartestEnergy and Low Carbon partner to accelerate UK's transition to net zero

The role of CfD and CPPAs in the UK PPA market

SmartestEnergy and AlphaReal partner to bring new CfD capacity to the UK market